Financial disorganization is a bigger problem than people think.

Key Points:

- When you’re disorganized, you have no idea how ‘good’ or ‘bad’ your financial situation is, until the bank calls. Or when your credit card gets rejected over dinner out

- You forget to schedule

- You fail to check details of contracts and employment agreements. You end up in a bad deal

- Behavioral scientists have several hypotheses about why people get so disorganized in taking care of even the simplest spending plan

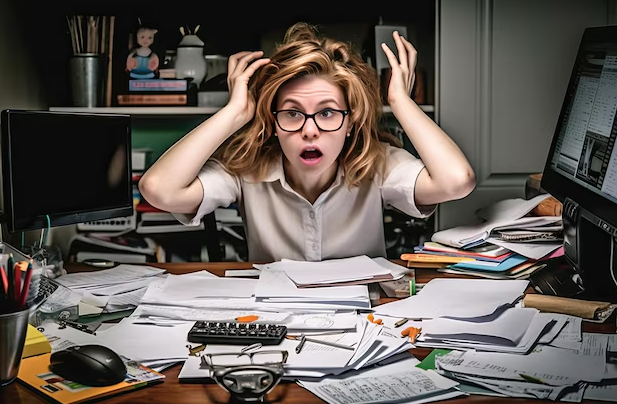

Learning how to deal with financial disorganization is a more widespread problem than people think. As measured by the volume of late fees paid to merchants, or the volume of provisioned payday loans, it appears that most of the world’s population is profoundly disorganized. I’m guilty of this as well. I have heaps of paperwork stacked up against my bookshelves, and have towers of paper on the floor in my office.

I know I’m disorganized, but I’ll do my best to explain this syndrome. Disorganized behavior, as defined by the American Psychological Disorganization Association is “behavior that is self-contradictory or inconsistent.” Often this includes acting against one’s best interest or engaging in self-sabotage.

Closer to home, when our environment is disorganized, so are we. Financial disorganization happens for many reasons and the consequences are worth thinking about. I address many of them in my book The Art and Science of Spending Less: Behavioral Observations on the Reckless Use of Everyday Money.

Here’s the impact of disorganization on financial recovery.

- When you’re disorganized, you lose bills that need to be paid that lead to late fees. You lose track of what you’re spending that leads to overspending.

- When you’re disorganized, you can’t plan so you can’t know how you’ll ever achieve your financial objectives. The disorganized life has consequences.

- You fail to check details of contracts and employment agreements. You end up in a bad deal.

- You shop for groceries but don’t bother to look at the expiry date on the back of the milk carton. You end up buying a sale item that shouldn’t be sold, is not drinkable and therefore you’ve wasted cash.

- When you’re disorganized, you don’t give yourself enough time to complete important tasks. Instead, you might rush through them and make mistakes.

- Unexpected things happen because you didn’t pre-think what could. You forgot to schedule.

- You have no idea how ‘good’ or ‘bad’ your financial situation is, until the bank calls. Or your credit card gets rejected over dinner out.

- You fail to fully accept that the mundane habit of paying bills on time violates your commitment to financial budgeting as well as your wellbeing.

Getting organized has many great benefits for your financial self. When you understand the reasons why you’re disorganized, you can do something about it. Behavioral scientists have several hypotheses about why people get so disorganized in taking care of even the simplest budget:

Extreme thinking and an obsession with being perfect

People think that record keeping must be scratch perfect. (No, it doesn’t). Paying bills on time, setting a budget and following it and arranging paperwork is fundamentally what’s required. It doesn’t require a perfectionist’s habit of paying bills on the exact date. Pay so long as it’s done before late charges are triggered.

Creating a budget needn’t be elaborate; a simple four column document will suffice. You can put a lot down on just one sheet of paper. Arranging your paperwork e.g., bills, invoices, receipts and loose papers in one spot needn’t become an ordeal. Put them all into a shoe box or a delivery container.

Lack of insight and skills

Behavioral science suggests that new skills and the insights that result from new skills go a long way towards improving shopping and debt management. Many skills can be learned.

Beliefs

Attitudes and beliefs are part of our cognitive machinery and when we are disorganized in our thinking, we are not thinking logically or ‘straight.’ How and what we think precedes what we do. Cognition precedes action. So, if we believe that having a closet full of expensive clothes makes us whole, then we are going to go out and spend lots of money on clothing (possibly that we’re likely never to wear or enjoy.) The mere act of ‘having’ them convinces ourselves we’ve made the right decision. But have we?

Indecision

Delaying important money decisions is a form of procrastination that has a direct relationship with disorganization. We delayed finding a shoebox for all our bills. We can’t seem to set up a simple filing system.

References:

- Almenberg, J., Lusardi, A., Säve‐Söderbergh, J., & Vestman, R. (2021). Attitudes towards debt and debt behavior. The Scandinavian Journal of Economics.

- Kotzé, L., & Smit, A. (2008). Personal financial literacy and personal debt management: the potential relationship with new venture creation. The Southern African Journal of Entrepreneurship and Small Business Management.

- Kennedy, B. P. (2013). The theory of planned behavior and financial literacy: A predictive model for credit card debt?.

References:

- Kotzé, L., & Smit, A. (2008). Personal financial literacy and personal debt management: the potential relationship with new venture creation. The Southern

About the Author:

MATT DRUCKER, D. Psych., is the founder of The Consumer Money Lab, an integrated research network in Australia. The Consumer Money Lab studies consumer financial behavior and how and why people spend money.

For more information, go to www.conversationwithmattdrucker.com